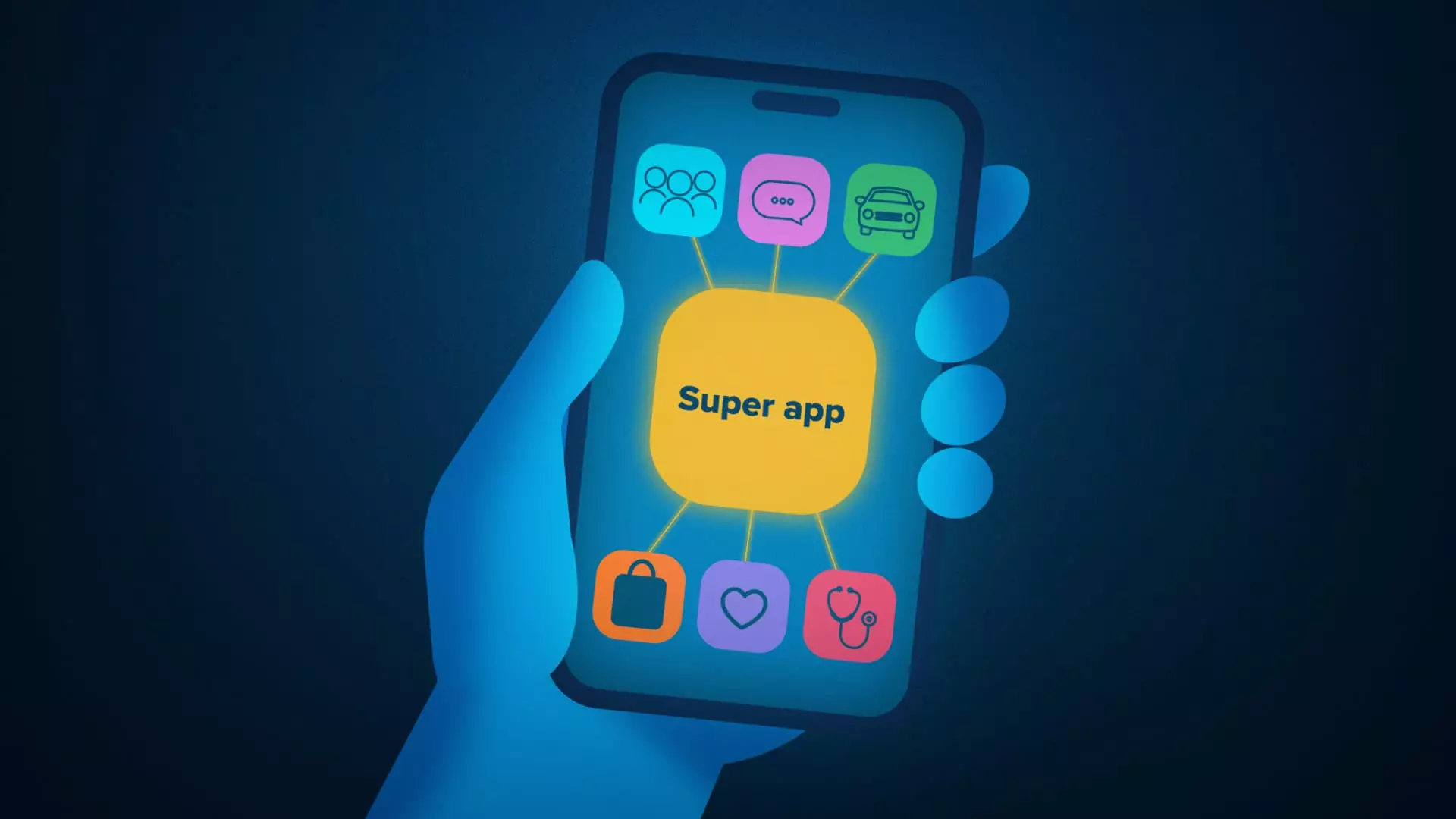

In today’s digital landscape, the average smartphone user juggles numerous applications, each designed to address specific needs. Recent studies indicate that Americans utilize roughly 46 different mobile apps each month for a range of daily activities. This constant switching between various platforms can be tedious and inefficient, prompting the desire for a centralized solution. Enter the concept of the “super app,” a multifaceted platform that combines multiple functionalities into one interface—enabling users to socialize, shop, handle finances, and communicate with healthcare professionals all from a single application.

The primary appeal of super apps lies in their ability to streamline daily tasks. As noted by tech experts, the convenience and integrated experience they offer is a significant draw for users frustrated by app congestion. Platforms like WeChat, which initially launched as a messaging service, have diversified their services to encompass everything from financial transactions to social networking, attracting over 1.3 billion active users globally. This integration not only enhances user experience but also fosters a sense of community, as users can connect and interact within a unified ecosystem.

Despite the evident advantages, the proliferation of super apps faces considerable hurdles, particularly in Western markets. Dan Prud’homme, an assistant professor at Florida International University, points out that the regulatory landscape in the U.S. poses significant challenges for super app development. The stringent regulatory environment includes strict consumer protection laws aimed at peer-to-peer lending, data privacy, and antitrust concerns. These regulations deter potential developers from creating all-encompassing applications akin to WeChat. Consequently, the pace at which super apps gain traction in the U.S. lags behind their Asian counterparts.

However, recent trends suggest that the tide may be turning. Major technology companies are increasingly exploring the possibility of introducing super app models tailored to the U.S. market. As consumer behavior evolves and the demand for convenience rises, there is a burgeoning opportunity for developers to create robust super apps that can successfully navigate regulatory challenges. The question remains whether the unique cultural and legal environment in the U.S. will allow such apps to flourish similarly to their Asian predecessors.

The evolution of super apps stands at a crucial juncture. As technology companies and consumers grow more accustomed to the convenience these platforms offer, the potential for a comprehensive “everything app” could reshape the digital landscape. Observers will be keen to see how regulations adapt to accommodate innovation in this space while still maintaining necessary consumer protections. If these advancements can be harmonized, we may soon witness the advent of super apps facilitating an unprecedented level of convenience in American consumers’ daily lives.